Credit Guarantee Scheme for Microfinance Institutions 2.0 (CGSMFI-2.0)

Why in News?

The Government of India has approved the extension of the Credit Guarantee Scheme for Microfinance Institutions 2.0 (CGSMFI-2.0) till 31 August 2026 or until guarantees worth ₹20,000 crore are issued, whichever is earlier. The maximum loan limit for large MFIs has also been increased significantly to improve credit availability for the microfinance sector.

What is CGSMFI-2.0?

CGSMFI-2.0 is a government-backed credit guarantee scheme launched in March 2026 to facilitate credit flow to Microfinance Institutions (MFIs) and NBFC-MFIs.

The scheme provides guarantee coverage to Member Lending Institutions (MLIs) such as banks and financial institutions that lend to MFIs. These institutions then extend microfinance loans to eligible low-income borrowers.

Objective

- Improve credit access for underserved borrowers.

- Strengthen the microfinance ecosystem.

- Promote financial inclusion.

- Support livelihood generation and rural entrepreneurship.

Key Features of CGSMFI-2.0

Differential Guarantee Coverage

Unlike the earlier scheme that provided a flat guarantee coverage, CGSMFI-2.0 adopts a differentiated approach.

| Category of MFI | Guarantee Coverage |

|---|---|

| Small MFI | 80% |

| Medium MFI | 75% |

| Large MFI | 70% |

This approach provides greater support to smaller institutions that often face higher financing constraints.

Classification of MFIs

MFIs are categorized based on their Assets Under Management (AUM).

| Category | AUM |

| Small MFI | Less than ₹500 crore |

| Medium MFI | ₹500 crore to less than ₹2,000 crore |

| Large MFI | ₹2,000 crore and above |

Revised Loan Limits

The scheme links loan eligibility to the size of the MFI.

| Category | Maximum Loan Limit |

| Small MFI | ₹100 crore |

| Medium MFI | ₹200 crore |

| Large MFI | ₹1,000 crore* |

*Recently increased from ₹300 crore to ₹1,000 crore, subject to an overall ceiling of 20% of AUM.

Equitable Credit Distribution

To ensure balanced credit flow:

- At least 5% of total loans must be extended to small MFIs.

- At least 10% must be extended to medium MFIs.

This prevents concentration of credit among large institutions.

Loan Conditions

- Loans must be disbursed within three months.

- Maximum tenure: Three years.

- Includes a one-year moratorium period.

- Funds can be used only for incremental lending to eligible borrowers.

Implementation Mechanism

The scheme operates through the:

National Credit Guarantee Trustee Company Ltd. (NCGTC)

Functions:

- Provides guarantee coverage.

- Processes approvals through an automatic mechanism.

- Facilitates faster loan sanction and disbursement.

This reduces risk for lenders and encourages greater participation in microfinance financing.

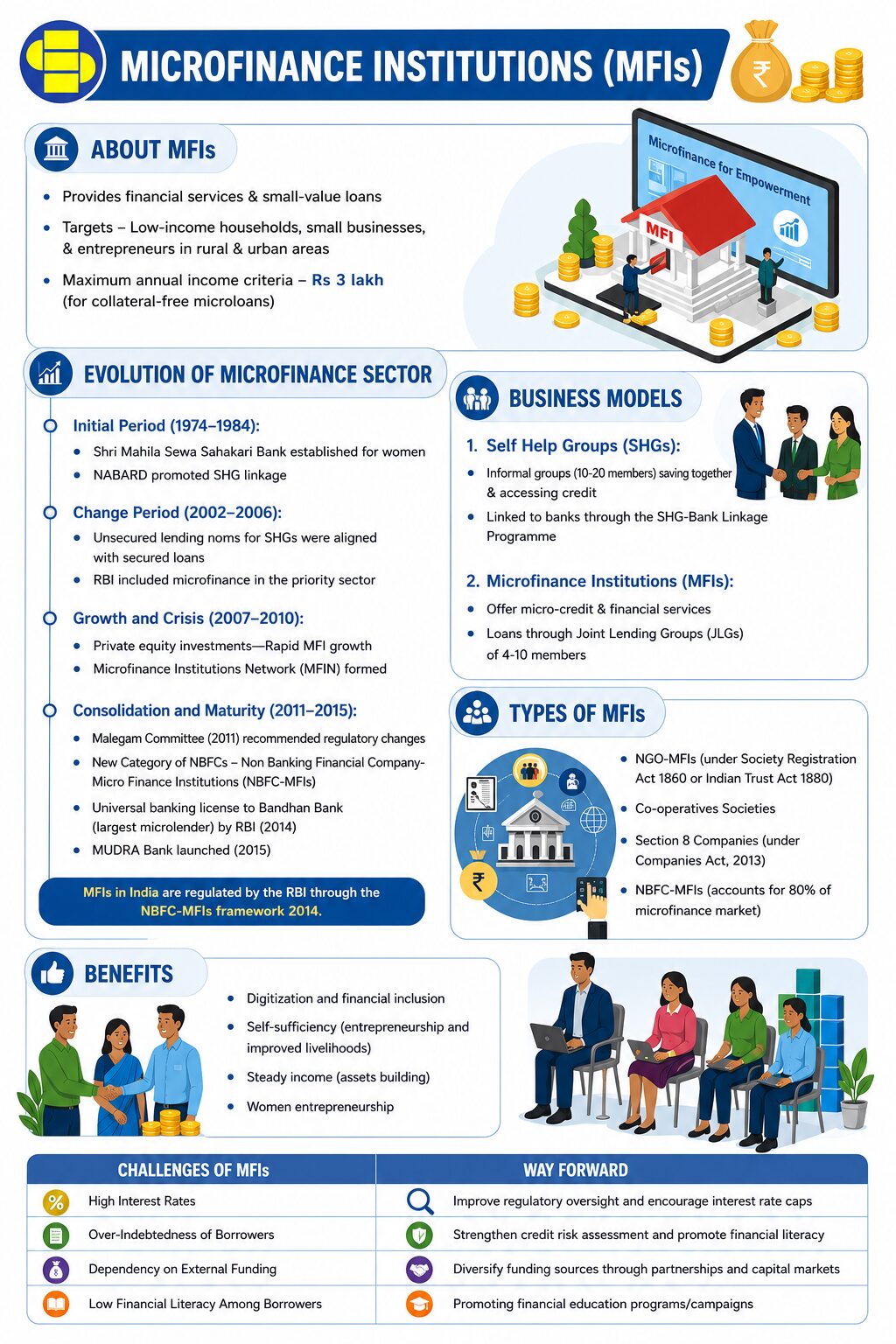

What are Microfinance Institutions (MFIs)?

Microfinance Institutions are specialized financial intermediaries that provide small loans and financial services to low-income households, particularly in rural and semi-urban areas.

Objectives

- Financial inclusion.

- Poverty reduction.

- Women empowerment.

- Livelihood generation.

- Entrepreneurship development.

Key Features of MFIs

| Feature | Details |

| Target Group | Low-income households and women |

| Loan Size | ₹5,000 to ₹1,00,000 |

| Collateral | Usually not required |

| Purpose | Income generation, consumption, emergencies |

Delivery Models

Joint Liability Group (JLG)

- Borrowers form groups.

- Group members share repayment responsibility.

Self-Help Group (SHG)

- Community-based model.

- Often linked with banks under the SHG-Bank Linkage Programme.

Regulatory Framework for MFIs

Reserve Bank of India (RBI)

Regulates NBFC-MFIs through:

- Prudential norms.

- Loan eligibility criteria.

- Regulatory guidelines.

NABARD

Supports microfinance through:

- Refinance assistance.

- SHG-Bank linkage programmes.

- Capacity building initiatives.

Significance of CGSMFI-2.0

Strengthening Financial Inclusion

The scheme improves access to formal finance for vulnerable and underserved communities.

Supporting Rural Economy

Microfinance credit helps:

- Small businesses.

- Self-employment.

- Agriculture-related activities.

- Women’s enterprises.

Reducing Credit Risk

Government-backed guarantees encourage lenders to provide credit to MFIs with greater confidence.

Promoting Inclusive Growth

The scheme contributes to:

- Poverty alleviation.

- Livelihood enhancement.

- Rural development.

Related Schemes and Institutions

Pradhan Mantri Mudra Yojana (PMMY)

Provides collateral-free loans to micro and small enterprises.

Deendayal Antyodaya Yojana – National Rural Livelihoods Mission (DAY-NRLM)

Promotes SHGs and rural livelihoods.

NABARD

Supports rural credit and financial inclusion.

NCGTC

Implements various government-backed credit guarantee schemes.

Credit Guarantee Scheme for Microfinance Institutions 2.0 (CGSMFI-2.0) Prelims Facts

| Topic | Fact |

| CGSMFI-2.0 Launch | March 2026 |

| Extended Till | 31 August 2026 |

| Implementing Agency | NCGTC |

| Regulator of NBFC-MFIs | RBI |

| Small MFI AUM | Less than ₹500 crore |

| Medium MFI AUM | ₹500 crore–₹2,000 crore |

| Large MFI AUM | ₹2,000 crore and above |

| Highest Guarantee Coverage | 80% (Small MFIs) |

Don’t Forget

CGSMFI-2.0 is a government-backed credit guarantee scheme that provides guarantee coverage to lending institutions financing Microfinance Institutions, thereby improving credit flow to low-income and underserved borrowers.

Discover more from Srishti IAS

Subscribe to get the latest posts sent to your email.